FHA Loans

What is an FHA Loan?

An FHA loan is a mortgage loan that is insured by the Federal Housing Administration (FHA). Essentially, the federal government insures loans for FHA-approved lenders in order to reduce their risk of loss if a borrower defaults on their mortgage payments.

The FHA program was created in response to the rash of foreclosures and defaults that happened in 1930s; to provide mortgage lenders with adequate insurance; and to help stimulate the housing market by making loans accessible and affordable. Nowadays, FHA loans are very popular, especially with first-time home buyers.

What Are the Advantages of FHA Loans?

Typically an FHA loan is one of the easiest types of mortgage loans to qualify for because it requires a low down payment and you can have less-than-perfect credit. An FHA down payment of 3.5 percent is required. Borrowers who cannot afford a traditional down payment of 20 percent or can’t get approved for private mortgage insurance should look into whether an FHA loan is the best option for their personal scenario. Another advantage of an FHA loan is that it can be assumable, which means if you want to sell your home, the buyer can “assume” the loan you have. People who have low or bad credit, have undergone a bankruptcy or have been foreclosed upon may be able to still qualify for an FHA loan.

What Are the Disadvantages of an FHA Mortgage?

You knew there had to be a catch, and here it is: Because an FHA loan does not have the strict standards of a conventional loan, it requires two kinds of mortgage insurance premiums: one is paid in full upfront – or, it can be financed into the mortgage – and the other is a monthly payment. Also, FHA loans require that the house meet certain conditions and must be appraised by an FHA-approved appraiser.

Upfront mortgage insurance premium (MIP) — Appropriately named, this is an upfront monthly premium payment, which means borrowers will pay a premium of 1.75% of the home loan, regardless of their credit score. Example: $300,000 loan x 1.75% = $5,250. This sum can be paid upfront at closing as part of the settlement charges or can be rolled into the mortgage.

Annual MIP (charged monthly) —Called an annual premium, this is actually a monthly charge that will be figured into your mortgage payment. It is based on a borrower’s loan-to-value (LTV) ratio, loan size, and length of loan. There are different Annual MIP values for loans with a term greater than 15 years and loans with a term of less than or equal to 15 years.Loans with a term of greater than 15 Years and Loan amount < or =$625,000.

Loans with a term of greater than 15 Years and Loan amount < or =$625,000

- LTV less than or equal to 95 percent, annual premiums are 1.30%

- LTV above 95 percent, annual premiums are 1.35%.

Loans with a term of greater than 15 Years and Loan Amount >$625,000

- LTV less than or equal to 95 percent, annual premiums are 1.50%

- LTV above 95 percent, annual premiums are 1.55%

Loans with a term of 15 years or less and Loan amount < or =$625,000

- LTV less than or equal to 90 percent, annual premiums are .45%

- LTV above 90 percent, annual premiums are .70%

Loans with a term of 15 Years or less and Loan Amount >$625,000

- LTV less than or equal to 90 percent, annual premiums are .70%

- LTV above 90 percent, annual premiums are .95%

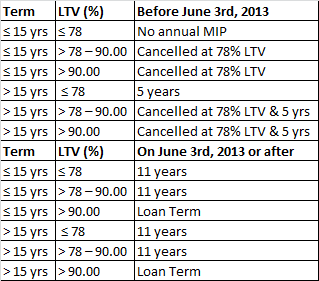

Example (for LTV less than 95 percent on a 30 year loan): $300,000 loan x 1.30% = $3,900. Then, divide $3,900 by 12 months = $325. Your monthly premium is $325 per month. The Mortgage Insurance will be in your payments for the entire loan term if your LTV is >90%. If your LTV is = or < 90%, the Mortgage Premium will be for the mortgage term or 11 years, whichever occurs first.

Single family home mortgages with amortization terms of 15 years or less, and a loan-to-value (LTV) ratio of 78 percent or less, remain exempt from the annual MIP.

FHA Mortgage Insurance Duration

The duration of your annual MIP will depend on the amortization term and LTV ratio on your loan origination date. Please refer to this chart for more information:

FHA Loan Requirements

- Must have a steady employment history or worked for the same employer for the past two years

- Must have a valid Social Security number, lawful residency in the U.S. and be of legal age to sign a mortgage in your state

- Must make a minimum down payment of 3.5 percent. The money can be gifted by a family member.

- New FHA loans are only available for primary residence occupancy

- Must have a property appraisal from a FHA-approved appraiser

- Your front-end ratio (mortgage payment plus HOA fees, property taxes, mortgage insurance, home insurance) needs to be less than 31 percent of your gross income, typically. You may be able to get approved with as high a percentage as 46.99 percent. Your lender will be required to provide justification as to why they believe the mortgage presents an acceptable risk. The lender must include any compensating factors used for loan approval.

- Your back-end ratio (mortgage plus all your monthly debt, i.e., credit card payment, car payment, student loans, etc.) needs to be less than 43 percent of your gross income, typically. You may be able to get approved with as high a percentage as 56.99 percent. Your lender will be required to provide justification as to why they believe the mortgage presents an acceptable risk. The lender must include any compensating factors used for loan approval.

- Minimum credit score of 580 for maximum financing with a minimum down payment of 3.5 percent.

- Minimum credit score of 500-579 for maximum LTV of 90 percent with a minimum down payment of 10 percent. FHA-qualified lenders will use a case-by-case basis to determine an applicants’ credit worthiness.

- Typically you must be two years out of bankruptcy and have re-established good credit. Exceptions can be made if you are out of bankruptcy for more than one year if there were extenuating circumstances beyond your control that caused the bankruptcy and you’ve managed your money in a responsible manner. See this page for more details.

- Typically you must be three year out of foreclosure and have re-established good credit. Exceptions can be made if there were extenuating circumstances and you’ve improved your credit. If you were unable to sell your home because you had to move to a new area, this does not qualify as an exception to the three-year foreclosure guideline.

Property needs to meet certain standards: Also, an FHA loan requires that a property meet certain minimum standards at appraisal. If the home you are purchasing does not meet these standards and a seller will not agree to the required repairs, your only option is to pay for the required repairs at closing (to be held in escrow until the repairs are complete).

FHA Loan Limits

There are maximum mortgage limits for FHA loans that vary by state and county. In certain counties, you may be able to get financing for a loan size up to $729,750 with a 3.5 percent down payment. Conventional financing for loans that can be bought by Fannie Mae or Freddie Mac are currently at $625,000.

How Do I Get an FHA Loan?

You can shop for mortgage quotes for an FHA loan on our website. Apply now.